THE MACRO CURRENT™

The Weekly Signal S6 | April 2026

When Liquidity Becomes the Constraint

Understanding how a supply shock evolves into funding stress—and what history suggests comes next

The Signal

The pressure has moved beyond energy.

It is now showing up in funding.

U.S. allies—particularly in the Gulf and parts of Asia—have sought access to U.S. dollar swap lines. Treasury Secretary Scott Bessent has acknowledged these requests in recent remarks, framing them as efforts to stabilize dollar funding markets and avoid disorderly selling of U.S. assets.

That framing is correct.

It is also revealing.

Swap lines are not routine tools. They are activated when access to dollars tightens and private markets cannot clear demand without destabilizing prices.

The shock has migrated.

From supply chains to balance sheets.

The Mechanism

The sequence is familiar, even if the trigger is not.

Energy Shock → Supply Constraint

Disruptions through the Strait of Hormuz tightened oil and LNG flows. Prices rose. More importantly, delivery became uncertain—timing slipped, insurance costs rose, and inventories failed to rebuild at normal speed.

Supply Constraint → Demand Adjustment

Higher input costs moved through food, transport, and manufacturing. Households pulled back at the margin. Firms delayed hiring and capex. The adjustment was gradual—less a drop than a loss of momentum.

Demand Adjustment → Liquidity Stress

As growth expectations softened and trade flows slowed, demand for U.S. dollars increased. Countries reliant on dollar funding to manage imports, service debt, and stabilize currencies faced tighter conditions.

That is when swap lines appear.

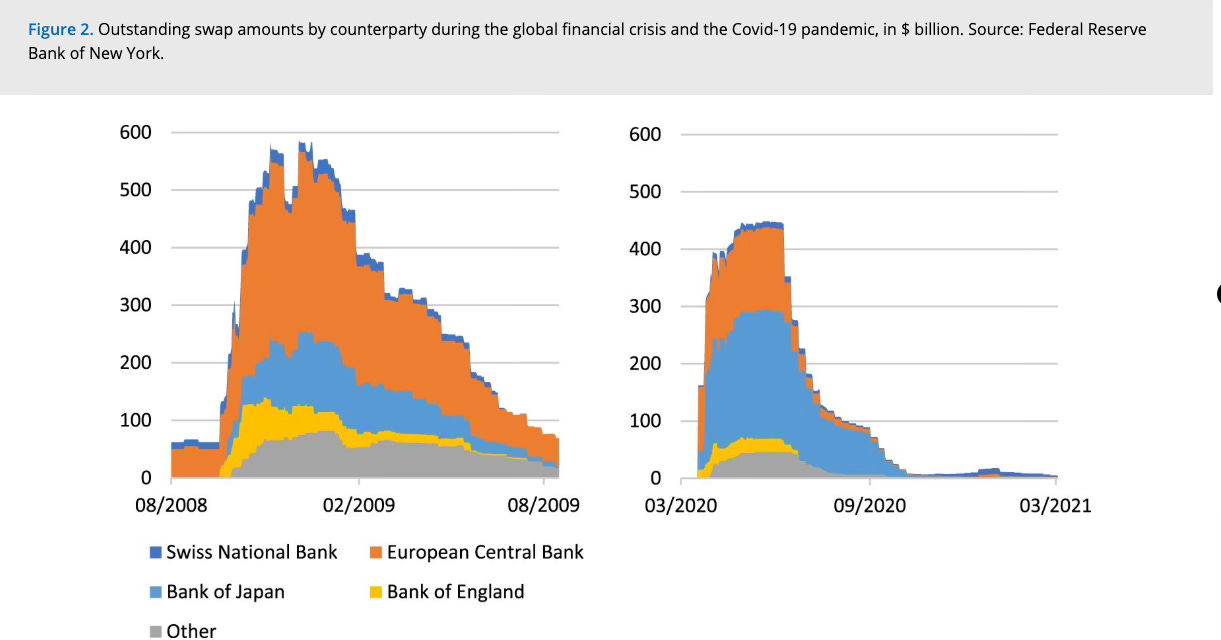

What Swap Lines Signal

Currency swap lines allow central banks to obtain U.S. dollars in exchange for local currency, providing emergency liquidity to domestic banks and markets.

They are crisis instruments.

Their modern use follows a clear pattern:

September 2008: After the failure of Lehman Brothers, dollar funding markets froze. The Federal Reserve expanded swap lines to major central banks to prevent a systemic liquidity collapse.

March 2020: During the initial COVID shock, a global dash for dollars forced the Fed to reopen and broaden swap lines to stabilize funding markets.

In both cases, the signal was the same:

Private dollar liquidity had become insufficient.

The public sector stepped in to keep the system functioning.

The Framework

This cycle combines elements of both episodes—with a different origin.

The constraint is not primarily financial. It is physical—energy, infrastructure, and logistics.

But once physical constraints persist, they transmit into financial conditions.

Supply tightens.

Demand adjusts.

Liquidity follows.

Policy is then forced to respond—not to stimulate growth, but to preserve functioning.

Structural Implication

Requests for swap lines mark a transition.

From economic adjustment

to financial strain.

Historically, when multiple countries seek dollar liquidity simultaneously, global financial conditions are tightening and growth is weakening.

The pattern is not deterministic.

It is consistent.

Two paths follow from here:

Stabilized Strain

Swap lines and partial normalization in energy flows keep markets functioning. Growth slows, but disorder is contained.

Escalating Tightness

Energy constraints persist. Dollar demand rises. Funding stress spreads across markets, accelerating the slowdown.

Closing Observation

We have seen this sequence before.

Supply shock.

Demand adjustment.

Liquidity stress.

The difference now is the source and the backdrop—physical constraints, higher debt, and weaker coordination.

That narrows the margin for policy to offset shocks without creating new ones.

The question is not whether stress exists.

It is whether it can be contained.

Because when liquidity becomes the constraint, the system does not stop.

It tightens.

And what ultimately determines the outcome is whether it can continue to function

consistently, and reliably.

The Macro Current

Where economics, technology, and institutions converge.